Introduction[1]

The Sustainable Development Goals (SDGs) have given new drive and focus to sustainable finance and investing with impact. They create an ambitious agenda to reduce poverty by 2030 with an equally ambitious agenda to finance them. Developed by policymakers worldwide, the SDGs include 17 goals concerning areas such as agriculture, infrastructure, health, and education in a drive to achieve gender equality, end hunger, build resilient infrastructure, among others. Ten of the 17 SDGs have a climate change aspect.

An enormous amount of financing is needed to achieve the SDGs – estimated at US$5 to US$7 trillion per year, with an estimated US$2 to US$3 trillion of that needed from the private sector. The SDGs put the spotlight on mobilizing finance from private resources to levels unheard of in the past.

The funds are in the global financial system. The challenge is getting them to where they are needed. Positively and importantly, the timing of the SDGs coincides with a heightened interest among investors worldwide to have greater impact in their investments. A growing number of asset managers are using the SDGs to frame their investment strategies and impact goals, making it easier for them to communicate with investors.

The size, scale, and speed involved in financing the SDGs will require transforming financial systems in emerging market countries (EMCs). That raises many opportunities and also potential risks, which financial market authorities will need to carefully balance. Together with other country leaders, they will need to determine how far and fast the financial system can evolve, given its starting point and the particular set of opportunities and risks the SDGs present.

Objectives

This note provides an overview to:

- How the SDGs and sustainable finance have evolved

- Key ways financial markets in EMCs may need to change to better mobilize the private financing needed

- Actions financial market authorities can focus on to accelerate the growth of financial systems in ways that allow them to take advantage of the opportunities while managing the risks that financing the SDGs present

Evolution to the SDGs and Investing with Impact

The two trends – of SDGs as the pathway for development and of investing with impact, have been paralleling one another, driven to some extent by similar concerns about the world’s future.

Creating an Agenda for Sustainable Development and Finance

Three interrelated agreements were signed in 2015 by governments around the world to accelerate financing for sustainable development and the SDGs:

- The Addis Ababa Financing for Development Agreement, adopted July 2015. Countries agreed on actions to “overhaul” global finance practices and generate investments to address a wide range of economic, social, and environmental challenges. The agreement provided the foundation for implementing the SDGs and Paris Climate Accord.

- The Sustainable Development Goals were adopted September 2015 by world leaders. The SDGs lay out an agenda for eliminating poverty by 2030 through 17 goals and 169 targets that address poverty, inequality, environmental degradation and gender equality to achieve prosperity, peace and justice. They touch on issues of health, infrastructure, agriculture, water quality, and education, with cross-cutting themes of economic growth, climate change, and sustainable cities (see Table 1). Countries are to set plans and programs for implementing the SDGs.

- The Paris Climate Accord, adopted December 2015, is an agreement among 195 countries to combat climate change and reach acceptable global temperature targets. Signatories are required to make best efforts through “nationally determined contributions” (NDCs) and report regularly on their contributions, with collective progress to be assessed every 5 years.

Many of the SDG goals are not new for EMCs. The critical difference is the intensity, urgency, and scale with which they are being pursued, the level of financing needed, and the high reliance on private sources. The link to climate change adds urgency and risks, as discussed below.

The Parallel Rise of Sustainable Finance and Investing with Impact

The need for private sources to play a central role in financing the SDGs is happening at a time when private investors, including pension funds, insurance firms, and individuals, are becoming increasingly intent on using their funds to invest with purpose and impact.

What is sustainable finance and investing with impact? Three investment approaches fall under the heading of “sustainable finance”:

- Socially Responsible Investing (SRI) refers to investing using negative screens to prohibit investment in areas such as tobacco, firearms, and other activities that an investor believes have negative implications for society.

- Environmental, Social, and Governance (ESG) Investing incorporates a broad set of ESG factors. Specific investments are not prohibited, but rankings are assigned to ESG factors for a company as part of the investment decision process.[2]

- Impact Investing refers to investing to have a positive purpose – to help solve social and environmental problems. The term was first used about 10 years ago. Early impact investors were willing to take concessionary financial returns to have impact. Today, impact investors span the spectrum of risk/return profiles, from investors willing to accept concessionary returns as a tradeoff for doing good to more mainstream investors seeking impact with market returns and others in between.[3] More recently, mainstream investors like BlackRock and Morgan Stanley have created impact investing arms.

About US$23 trillion of global assets are professionally managed using sustainable investment strategies. While this represents a 25% increase since 2014, it is small compared to the total amount of funds needed to support the SDGs, and only represents about 26% of professionally managed assets globally, indicating there is considerable scope for growth.[4] Sustainable investing’s market share has grown in all regions except Europe (because Europe tightened its definition of sustainable investing).[5]

The growing use of sustainable investment strategies is largely due to investor activism. Investors are pushing asset managers to “do good” with their money and to offer related investment products. Millennials are one source of pressure, looking to create a better future to grow old in, suggesting that this is not a fad but a shift.

The Paris Climate Accord and SDGs have given more drive and focus. A growing number of asset managers and corporations are using the SDGs to strategize and articulate their impact – making it easier for them to communicate their strategies and goals to investors and to measure whether they have been achieved.[6]

A large discussion has been around whether there is a tradeoff between financial return and investing with impact in one of these forms. The OECD reports that a growing number of studies show that companies with improving ESG scores outperform the broader market, especially in EMCs. Another study shows that using ESG factors to evaluate an emerging market investment can lead to investments that outperform because it signifies that the investee is well managed.[7]

Global Initiatives to Support Financing for the SDGs

Given the significant challenges of the SDGs, many global initiatives and collaborations have sprung up – some public, some private, some mixed – to share information, perspectives, and ideas. These are discussed more below.

Implications for Financial Markets in EMCs

The scale and urgency of SDG financing and the need to mobilize trillions of dollars particularly from private sector investors raises significant challenges to build the appropriate financial systems in emerging market countries. It creates many opportunities and potential risks from expanded activities and the strong link to climate change.

Climate change creates both physical and transitional risks. Threats from extreme weather events associated with climate change can debilitate economies, causing corporate devaluations and bankruptcies, loss of homes and employment, and other economic dislocations that have serious affects for financial institutions and markets.[8] In addition, the transition to more climate-friendly operations can create “stranded assets”, assets that lose value because they are associated with declining business areas, negatively affecting companies and their financiers.

There are several cross-cutting as well as institution-specific actions that will help build the local financial markets needed in EMCs. Of course, a country’s starting point – most notably the size and sophistication of its financial markets and services and investor base – will influence how far and fast change can happen.

Cross-Cutting Needs

Expanded Financial Instruments. The types of financing needed and of investors required to provide that financing creates a demand for new financial instruments in EMCs. The most important elements are:

- Risk-mitigation structures. Given the relative inexperience and social-security role of many investors, particularly pension and insurance entities, as well as their fiduciary need to provide sufficient financial returns, countries will need to offer instruments that allow investors to create the risk/return profile that suits their operations. Among the most important structural features are:

- Asset-backed securities and securitization – These include covered bonds, mortgage-backed securities for commercial and retail borrowers, and toll road receivables and securitizations. They are equally attractive to borrowers because they allow revenues from the underlying operations to finance the security.

- Guarantees and first loss provisions that serve to mitigate risks

- Investment Funds – listed (Exchange Traded Funds) or unlisted, public and private, provide diversification and professional management.

- Thematic bonds. Thematic bonds are another important instrument to help funnel investments to target areas. Green bonds are the most prominent example, but social and gender bonds are growing as well. The Green Bond market has more than tripled in the past 5 years, from US$400 billion to an estimated US$1.45 trillion (see Chart 1). Improved market definitions, standards, and procedures, and proof that commercial returns are not being forfeited, has helped accelerate that growth.[9]

- ESG Indices. ESG indices help standardize ESG reporting approaches. They help investors benchmark to ESG investment performance and compare the ESG standing of different investment options.

The ability to create blended finance transactions is critical to achieving the SDGs. Blended finance helps catalyze private financing by strategically using funding from public and/or philanthropic sources – entities willing to take lower returns and/or higher risks – in innovative ways that create an investment which appeals to private investors. Mitigating risk through guarantees or first loss positions and taking lower returns in a fund or other type of investment to allow private investors to achieve higher yields are some approaches used (see Box 1).[10] [11]

Use of these instruments has grown in some EMCs but is still at early stages in many others. As Chart 2 shows, green bonds have grown dramatically in the past five years, but only a handful of EMCs (most notably China and India) have markets of any size. Many countries still need improved frameworks for risk-mitigation instruments like asset-backed securities to grow. Many stock exchanges and investment firms have created ESG indices covering EMC companies, including London’s FTSE4Good, Bombay Stock Exchange’s Greenex, Johannesburg Stock Exchange’s SRI Index, and Morgan Stanley’s MSCI Emerging Markets ESG Leaders Index.

Significantly Enhanced Disclosure and Information. The need for disclosure related to SDG activity, particularly around climate change, cannot be overstated. As a start, investors want to make sure that their money is being used for the intended purpose. In addition, social and environmental risks and challenges are widely seen to be increasing. Information needs to be available about a firm’s exposures and their ability to identify, assess, and manage the risks – not just for the investor but for the firm borrowing the money as well.

Standardized, reliable information will be needed even more so than in the past – by investors to make informed investment decisions about risk, pricing, and valuation, to compare investment opportunities, and to create viable tools like ESG indices; by companies and financial institutions to identify and manage their own risks today and into the future; and by regulators to create safe, sound, and credible marketplaces.

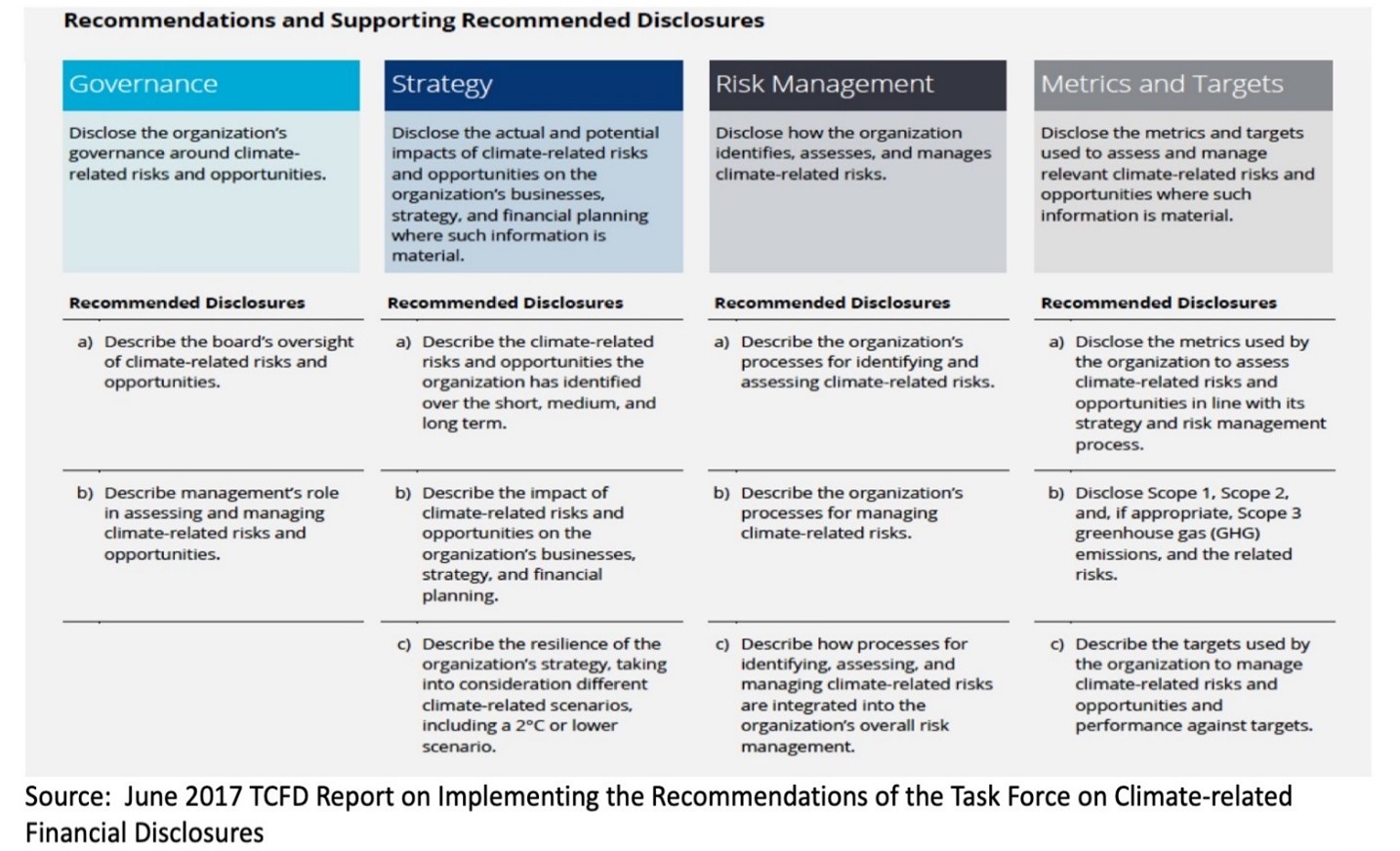

Given the critical importance of disclosure, the Financial Stability Board (FSB), at the request of the G20 Finance Ministers, created The Task Force on Climate-Related Finance Disclosures (TCFD).[12] The TCFD is an industry led initiative charged with developing voluntary recommendations on how to integrate climate related financial disclosures into mainstream reporting. The recommendations apply to investors, businesses, and financial institutions. The accompanying report includes an annex on how to implement the recommendations.

TCFD created a framework focused on four areas – governance, strategy, risk management, and metrics and targets – and recommends disclosures for each (see Table 2). These disclosures provide insights into how a firm can help ensure it has: (1) processes to assess the opportunities and risks being taken which include the board and top management; (2) leadership which understands their impact and works it into the firm’s strategy, (3) processes for identifying and managing the risks; and (4) metrics and targets to assess and manage them. While the TCFD focuses on climate change, aspects of its framework can be adopted for other ESG areas as well.

As of September 2018, over 500 institutions support the TCFD, including over 287 financial firms responsible for managing nearly US$100 trillion of assets.

Improved Risk Management Financial institutions will need to strengthen their risk management capabilities – to incorporate the full range of risks they will face and to be able to handle more complex risks. The UN reports that leading insurers are incorporating environmental risk factors in their insurance and investment strategies, but this is far from the norm.[13]

As of September 2018, over 500 institutions support the TCFD, including over 287 financial firms responsible for managing nearly US$100 trillion of assets.

Expanded Education and Collaboration. Given the rapid and significant changes needed to support SDG financing, education and collaboration among market participants as well as financial authorities will be critical to making progress and achieving success.

Domestically, sharing information and collaborating with other financial institutions, financial authorities, and relevant entities outside the financial sector, can accelerate thoughtful decision making and change. It can help ensure that participants remain on top of new developments and ideas. Banks and insurance entities hold extensive information and insights into local credit and risk conditions. They can be encouraged or required to share their non-proprietary information to inform and help optimize decision making by others.

Multi-stakeholder partnerships also can help private financial firms develop new pipelines of investable and sustainable deals, something they will need to actively do, by making it easier to pinpoint and address obstacles that come from outside the financial system.

Similarly, private firms can benefit from participating in international industry groups. The Sustainable Stock Exchange Initiative, the International Capital Markets Association’s (ICMA’s) thematic bond principles groups, the Climate Bonds Initiative are just some of the many international private sector groups working on ESG and SDG issues. Industry groups working with the UN have put together principles for responsible investing, for sustainable insurance, and recently drafted sustainable principles for banking (see Table 3). The principles lay out how financial institutions can align their business practices to support ESG goals and better communicate their achievements.

Industry associations and other groups can lead capacity building efforts on areas such as products and services development, risk management, and investment analysis in the new SDG context. ICMA’s working group on the green bond market principles illustrates that point.

Actions for Specific Financial Institutions and Markets

Institutional Investors. The focus on mobilizing private capital is on institutional investors, particularly pension funds and life insurance companies because of their potential size as well as need for long term assets, on sovereign wealth funds and strategic investment funds, which increasingly are investing domestically, and on certain mutual funds.

The ability of domestic institutional investors to invest sustainably and support the SDGs will be affected by many factors specific to their operations. The obvious starting point will be the amount of investable funds they have and the rate at which they are growing, as well as their level of experience and sophistication. This will vary considerably from one country to another and influence the role these investors can play at any point in time.

Taking those points into account, these investors will need to:

- Be allowed by regulation to invest in the types of areas included in the SDGs. Many emerging market investors, particularly insurance companies and pension funds, are constrained in their ability to hold “alternative investments.”

- Have access to data and research to make informed investment decisions

- Have the capacity and internal processes to evaluate, price, and manage the investment risks, which will be greater than in the past

- Be willing and able to invest long term, e.g., not be pushed into short-termism by short term performance benchmarks or liquidity requirements

- Be able to afford the costs of integrating sustainability factors into their operations

Most EMCs will need foreign resources. Growing numbers of foreign investors are looking for investments with impact in emerging markets. Countries will need several conditions to attract these investors, starting with the ability to access the market – e.g., enabling capital control and currency policies – and including market factors like the size, liquidity, and quality of transactions.

These are real challenges for many EMCs. Their institutional investors are often small with limited experience. Many play social security roles so are conservative by nature, as they should be. In addition, investors will be facing new investment risks related to the SDGs, including having to rely on evolving data and disclosure and the threat of “stranded assets” – e.g. assets in areas that are being marginalized or phased-out as the country shifts to more climate-related sustainable practices.

Banks. As appropriate for their role in emerging market financial systems, banks will need to continue to play a central role in funding the SDGs and providing sustainable finance. Consumer financing, mortgages across commercial and retail borrowers, and construction financing that provides the foundation for longer term infrastructure finance are just some of the areas requiring bank involvement. As noted, banks’ insights on credit and other risk characteristics can be shared with others.

To fully support the SDGs, banks will need to be able to:

- Lend where possible to areas like infrastructure and be able to take on selected long-term exposures. This will require that regulations do not unnecessarily constrain the ability to lend, through size, liquidity, or capital adequacy requirements. In some countries, underdeveloped bond markets will constrain longer term lending by reducing a bank’s ability to offset long term loans with long term funding, creating mismatches.

- Have the capacity and expertise to manage the new exposures, including risks from stranded assets. Stranded assets may be a special challenge for banks because of their central and significant role funding businesses that may face reduced demand and divestments because of less climate-friendly practices.

Insurance. Outside their role as investors, financing the SDGs raises sizable challenges for insurance companies.[14] As underwriters of risk, they are being looked at to provide more comprehensive coverage to improve health and safety, at a time when social demographics, natural disasters, and climate issues are increasing and becoming more complex. They are at the forefront in providing risk management and risk transfer to help create stability and sustainability.

Insurance is linked to a number of SDGs, directly and indirectly, including automobile, health, agriculture, infrastructure, at the retail, institutional, and national levels. Accelerating and deepening climate change events intensify the challenges.

The new landscape will require insurance entities to:

- Create products and services that are more accessible and affordable, particularly to lower-income women and men

- Be able to price insurance appropriately to adequately cover their exposures and build up sufficient reserves to withstand sizable claims

- Strengthen their risk management capacities to include ESG factors and to cover the added risks inherent in the SDGs

- Have and provide quality information and disclosure to manage their own operations and help inform those of others. The TCFD recommendations are a useful guide.

Today, insurance penetration is very low in many EMCs. The reason for that will need to be understood and addressed in each country. At the same time, insurance firms will have to balance the demand for expanded products and services and the goal of maintaining prudential standing.

Capital Markets. Capital markets and capital market development will need to play a larger role in most emerging market countries because these markets support the SDGs in two important ways:

- They provide many of the instruments needed by borrowers and investors. Much of what’s needed is long term, local currency financing through risk-mitigated and thematic products. These are often based on capital market instruments – e.g. asset-backed bonds, listed funds, green bonds and long-term local currency financing provided by bonds and equity more generally.

- They provide a core mechanism for disclosure and standard setting. Public securities markets, particularly through stock exchanges, provide a critical avenue for disclosing information to make informed investment decisions and setting definitions and standards to accelerate use of new products. They will be a primary vehicle for implementing TCFD recommendations.

Stock exchanges around the world are playing a growing role in moving the sustainable finance agenda forward, by setting definitions and standards, establishing good practice requirements, requiring disclosures, and creating new products for areas such as ESG and green bonds. The Sustainable Stock Exchange Initiative (SEE) has elevated stock exchanges to a leading role in this regard.[15] About 80 countries are part of the SSE, most from emerging markets. One recent development is the growing focus on using ESG approaches for fixed income products (i.e., bonds); ESG has traditionally been applied only to equity investments.

Developing local capital markets has been on the agenda for many EMCs for a long time. Despite that, many EMC capital markets are still underdeveloped outside the government bond markets. Equity markets are often concentrated; non-government bond markets are often small, shallow, and illiquid. As noted, the green bond market has grown dramatically in the aggregate but is still very small in most EMCs, partly reflecting constraints in the underlying bond markets. And as noted, many of the needed instruments are also not actively available. Underdeveloped capital markets will constrain availability of the sustainable finance needed for the SDGs.

These needs and challenges will be even more difficult to address in the least developed markets. They may have to take different approaches by determining where the longer-term investable funds in their financial system reside, how they might best be tapped, and by continuing to rely more extensively on concessionary/development financing.

Implications for Financial Market Authorities

Emerging market financial authorities have a fundamental and demanding role to play in creating a financial system that can support the SDGs with a large agenda of actions. This will include finding the right balance between embracing the opportunities and managing the risks, setting the scale and speed of change, and accelerating efforts to remove barriers that have stalled financial market development in the past.

There are many steps financial authorities can take. They break down into two groups: steps to enable market activity and steps to improve the quality of financial market oversight.

Enabling Market Activity

In terms of market activity, key areas of focus are to:

Strengthen the enabling environment. As noted, many EMCs do not have the range of instruments or level of institutional and market development needed to meet this challenge. Key areas to consider are:

- Institutional Investors – review investment regulations for investors like pension and insurance entities to see if they inadvertently or unnecessarily restrict investment in the SDGs or push investors into short-term instruments. Also review the pace at which investment assets are growing to determine if obstacles to growth exist that need to be addressed.

- Financial Instruments – review the ability to introduce and use instruments such as asset-backed products, guarantees, thematic bonds, indexes, and forms of blended finance, as well as the underlying bond and equity markets to address obstacles to their development. Problems in the underlying markets will constrain the ability to finance through them and to use more sophisticated variations like securitized bonds that are so critically needed. As noted, the ability to do blended finance transactions is especially important because of the role they can play in creating risk/return profiles that match private investor needs and mobilize their investment.

- Banking – review policies and regulations that affect bank exposures to SDG areas, and the ability to invest in structured products like covered bonds and asset-backed securities, and address ones that may be unnecessarily constraining. Also review the ability for banks to raise long term funds as that will affect their ability to invest long term without creating serious mismatch risks.

- Insurance –review the ability to introduce new insurance products and services and capabilities to set prices that reflect the risk insurance companies are assuming to identify areas and revise as appropriate.

Improve data and enhance disclosure. As discussed, improved data and greater disclosure are crucial for supporting the SDGs. Financial market authorities should work to implement the TCFD recommendations for climate change and consider using similar approaches for the entire ESG spectrum. While TCFD is voluntary, regulators should consider making it mandatory. Adjustments should be made as needed to suit country circumstances.

Financial authorities can formulate and support proposals to develop standardized investment terminology. They should also be clear on their position about ESG investment practices and their relationship to investor fiduciary responsibility. The growing consensus, as the OECD and others report, is that incorporating ESG factors into investment practices is an asset manager’s fiduciary responsibility because these factors can significantly influence future investment performance.[16]

Assure financial institutions have appropriate risk management practices and operations Risk management functions need to be able to accommodate new and more complex risks and have the ability to respond as needed.

Strengthening Financial Market Oversight

In terms of steps to strengthen their ability to oversee and regulate a rapidly changing marketplace, financial authorities can:

Develop updated approaches to financial market assessments to ensure they have a clear understanding of the landscape. This can include assessing the purpose, size, and type of financing needed to support the SDGs, the financing available in the financial system and in what form, and how to best evolve the financial system so the financing available supports the areas in need. The assessment could be undertaken in collaboration with other concerned governmental and private sector bodies. The information could be shared widely as it will provide useful insights for others as well.

Increase risk analyses at the systemic and firm levels. Significant risks can arise from the process of developing and transforming the financial system and from new exposures being taken on, again with climate change presenting a large one. Financial authorities will need to incorporate these elements into their risk analyses, evaluate the impact from macro to micro implications, and have plans for how to address them.

One new aspect that will need to be factored-in concerns “stranded assets”. A quick transition to new technologies and greener practices will reduce the physical effects of climate change and reduce related risks on insurance firms and investors. But it can also create credit downgrades, decreases in valuations and, potentially, defaults and bankruptcies among companies engaged in activities that are being phased out -- which can spill over and challenge their insurance firms and investors. Financial market authorities should be important contributors to discussions on the optimal transformation process.

In addition, financial market authorities can guide others on how to evaluate and manage complex risks. It will be critically important to ensure that private financial firms develop improved techniques to understand and quantify ESG risks, especially climate-related ones, given their high magnitude, uncertainty, and potential negative impact.

Strengthen supervision of financial markets and institutions. As is typically the case, the quality, clarity, and credibility of regulation and supervision will directly influence the market stability and confidence needed to mobilize private finance. Sound supervision takes on added importance in this context, given the need to reach higher levels of market size, liquidity, and transactions in shortened time frames.

Enhance education and capacity building. Education and capacity building will be needed across the board – from the financial authorities to financial service providers to investors. Authorities need to take steps to improve their own knowledge and capacity and can help create programs that strengthen those they supervise and those they work for and with.

Collaborate domestically and internationally. Given the scope and urgency of change involved, global plans to finance the SDGs have always emphasized the importance of cross-cutting collaboration and multi-stakeholder partnerships to achieve the best results. This is critical as much, if not more so, for financial authorities. They will benefit greatly if they:

- Collaborate domestically to bring the needed parties to the table. Banking, insurance, and capital market authorities need to work together to set shared goals and align policies. They also need to work with the financial services industry as well as stakeholders from other sectors that have influence on the broader picture (e.g. tax authorities, actors from the real sector being focused on). Cross-sectoral alliances will help streamline and accelerate the process of designing solutions that work from a prudential and market angle. Authorities should also ensure that private financial sector firms are collaborating amongst themselves.

- Collaborate internationally to take advantage of global initiatives to keep updated on new approaches and ideas and how to align with internationally-adopted practices. Many international groups of financial authorities, often together with industry leaders, are sharing experience and resources and creating principles and approaches – from the G20 and FSB to groups like the Sustainable Banking Network (SBN), Sustainable Stock Exchange Initiative, and Sustainable Insurance Forum. Standard setting bodies (such as the International Association of Insurance Supervisors (IAIS) and the International Organization of Securities Commissions (IOSCO) are other forums to work through.

Encourage government leaders to implement a national plan for achieving the SDGs and participate as needed. Countries are expected to create national plans for achieving the SDGs. National plans, particularly when led by a high-level visionary, will help bring cross-cutting parties to the table, unify agendas to a common goal, and provide guideposts for how to achieve them. They will indicate target areas and how to apply resources. They can provide the clarity and certainty investors need to make investment decisions. Several countries have or are working on national roadmaps for sustainability.

Conclusion

The SDGs present an ambitious and challenging agenda to improve the quality and safety of life for men and women throughout the world, and especially in the EMCs. They bring an equally ambitious and challenging agenda to strengthen and transform financial systems to mobilize new levels of private capital at new levels of scale and speed.

EMCs are at different stages of economic and financial sector development. Countries will have to determine what is best for their circumstances and what they believe they can reasonably achieve in different time frames – and how to mix concessionary development finance with government, IFI, and private sector funding. National plans can help clarify, articulate, and communicate this information and provide guideposts that will help all involved move forward.

Financial market authorities have a central and demanding role to play in this new context. They will want to have a clear, on-going understanding of the situation, create stronger enabling environments, expand and deepen the risk management assessments and capabilities of supervised firms, and importantly, ensure improved data and disclosure so investors have the information they need to make solid investment decisions.

Financial market authorities will want to ensure that the financial institutions they oversee are introducing and using analyses, risk management practices, and internal operations that reflect the demands of the new environment and to inform and engage with government colleagues and counterparts in the financial sector and beyond who play a role in securing results. Education and collaboration will be critical in this fast moving and ambitious environment. In addition to domestic efforts, financial authorities should take advantage of the many international resources and multi-stakeholder partnerships available and encourage the financial industry to as well.

Disclosure is a core piece of the puzzle not only for investors but for the companies and other financial institutions that produce it. The TCFD provides recommendations and implementation approaches that will help get the right information, transparency, and internal processes and procedures in place to support it. Its guidance is relevant for ESG beyond climate issues.

With the financial sector at the core of change, enhanced clarity, transparency, and overall strength of financial market authorities will raise market confidence and help catalyze the financing needed.

Key References

Business & Sustainable Development Commission and Convergence. The State of Blended Finance: Working Paper. July 2017. http://s3.amazonaws.com/aws-bsdc/BSDC_and_Convergence__The_State_of_Blended_Finance__July_2017.pdf

Organisation for Economic Co-operation and Development. Investment Governance and the Integration of Environmental, Social and Governance Factors. 2017.

https://www.oecd.org/finance/Investment-Governance-Integration-ESG-Factors.pdf

Sustainable Stock Exchange Initiative. How Stock Exchanges Can Grow Green Finance: A Voluntary Action Plan. 2017.

http://www.sseinitiative.org/wp-content/uploads/2017/11/SSE-Green-Finance-Guidance-.pdf

Task Force on Climate-related Financial Disclosures. Final Report: Recommendations of the Task Force on Climate-related Financial Disclosures. June 2017. https://www.fsb-tcfd.org/wp-content/uploads/2017/06/FINAL-2017-TCFD-Report-11052018.pdf

Toronto Centre. Climate Change. TC Note. July 2017. https://www.torontocentre.org/index.php?option=com_content&view=article&id=74:climate-change&catid=14&Itemid=101#:~:text=Climate%20Change&text=Toronto%20Centre%20provides%20high%20quality,advance%20financial%20stability%20and%20inclusion.

United Nations Environment Programme. Sustainable Insurance: The Emerging Agenda for Supervisors and Regulators. August 2017. https://www.unepfi.org/psi/wp-content/uploads/2017/08/Sustainable_Insurance_The_Emerging_Agenda.pdf

Additional Readings

Bank of England. Prudential Regulatory Authority. Transition in Thinking: The Impact of Climate Change on the UK Banking Sector. September 2018.

Bank of England. Prudential Regulation Authority. The Impact of Climate Change on the UK Insurance Sector. September 2015. https://www.bankofengland.co.uk/-/media/boe/files/prudential-regulation/publication/impact-of-climate-change-on-the-uk-insurance-sector.pdf?la=en&hash=EF9FE0FF9AEC940A2BA722324902FFBA49A5A29A

Climate Bonds Initiative. Bonds and Climate Change: The State of the Market 2018. September 2018.

Global Impact Investing Network. Achieving the Sustainable Development Goals: The Role of Impact Investing. September 2017.

https://thegiin.org/assets/GIIN_Impact%20InvestingSDGs_Finalprofiles_webfile.pdf

Global Impact Investing Network. Annual Impact Investor Survey 2018. June 6, 2018.

https://thegiin.org/assets/2018_GIIN_Annual_Impact_Investor_Survey_webfile.pdf

Global Sustainable Investment Alliance. 2016: Global Sustainable Investment Review. 2016.

http://www.gsi-alliance.org/wp-content/uploads/2017/03/GSIR_Review2016.F.pdf

Inderst, Georg and Stewart, Fiona. Incorporating Environmental, Social and Governance (ESG) Factors in Fixed Income Investment. World Bank Group, 2018.

Organisation for Economic Co-operation and Development. OECD DAC Blended Finance Principles for Unlocking Commercial Finance for the Sustainable Development Goals. January 2018.

Organisation for Economic Co-operation and Development, International Capital Markets Association, Climate Bonds Initiative, and Green Finance Committee of China Society for Finance and Banking. Green Bonds: Country Experiences, Barriers and Options. 2016. http://unepinquiry.org/wp-content/uploads/2016/09/6_Green_Bonds_Country_Experiences_Barriers_and_Options.pdf

International Institute for Sustainable Development. SDG Knowledge Hub. https://sdg.iisd.org/sdgs/

Sustainable Stock Exchanges Initiative. Climate, Carbon & Stranded Assets: What Do They Mean for Stock Exchanges? 2015. http://www.sseinitiative.org/wp-content/uploads/2015/12/SSE-Carbon-Tracker-Climate-Brief.pdf

Task Force on Climate-related Financial Disclosures. TCFD: 2018 Status Report. September 2018. https://www.fsb-tcfd.org/publications/tcfd-2018-status-report/

Task Force on Climate-related Financial Disclosure. TCFD Knowledge Hub. www.fsb-tcfd.org

United Nations Environment Programme. Fiduciary Duty in the 21st Century. 2015.

https://www.unepfi.org/fileadmin/documents/fiduciary_duty_21st_century.pdf

United Nations Environment Programme. Making Waves: Aligning the Financial System with Sustainable Development. April 2018.

http://unepinquiry.org/wp-content/uploads/2018/04/Making_Waves.pdf

United Nations Global Compact and KPMG. SDG Industry Matrix: Financial Services. September 2015.

https://home.kpmg/content/dam/kpmg/xx/pdf/2017/05/sdg-financial-services.pdf

United Nations Conference on Trade and Development (UNCTAD) and World Federation of Exchanges. The Role of Stock Exchanges in Fostering Economic Growth and Sustainable Development. Undated.

https://unctad.org/en/PublicationsLibrary/WFE_UNCTAD_2017_en.pdf

[1] This note was prepared by Alison Harwood on behalf of the Toronto Centre.

[2] The Principles of Responsible Investing (PRI), launched in 2006 by the UNEP Finance Initiative and the UN Global Compact, are a voluntary framework by which all investors can incorporate ESG issues into their decision-making and ownership practices and so better align their objectives with those of society at large. See www.unpri.org.

[3] The Global Impact Investor Network (GIIN)’s 2018 investor survey reported that 64% of respondents target risk-adjusted market returns. The remainder will accept below market returns, with 20% seeking returns closer to market and 16% closer to capital preservation. 229 firms responded representing US$228 billion in AUM. About 56% of those funds are invested in emerging markets.

[4] Global Sustainable Investment Alliance, 2016: Global Sustainable Investment Review, (2016), p. 3, http://www.gsi-alliance.org/wp-content/uploads/2017/03/GSIR_Review2016.F.pdf

[5] Ibid. GSIA uses an inclusive definition of sustainable investing that includes SRI, ESG, and impact investing. The 2016 report introduced new sustainable investment forums in Latin America and Africa that are gathering and contributed information to the GSIA’s 2016 review.

[6] Many corporations are selecting particular SDGs to focus and articulate their strategy, often in response to consumer pressure. That pushes change throughout their supply chains and in turn effects financial transactions.

[7] Organisation for Economic Co-operation and Development, Investment Governance and the Integration of Environmental, Social and Governance Factors, (2017), https://www.oecd.org/finance/Investment-Governance-Integration-ESG-Factors.pdf. See also Reshma Kapadia, “ESG Investing in the Emerging Markets is Tough, but Lucrative,” Barrons (June 8, 2018), www.barrons.com.

[8] Toronto Centre, Climate Change, TC Note (July 2017), https://www.torontocentre.org/index.php?option=com_content&view=article&id=74:climate-change&catid=14&Itemid=101#:~:text=Climate%20Change&text=Toronto%20Centre%20provides%20high%20quality,advance%20financial%20stability%20and%20inclusion., provides a full discussion of the risks associated with climate change and the financial sector implications.

[9] Gender bonds are issued to finance companies that promote gender equality. The market is developing, with issues by banks such as Canada’s CIBC (C$1billion) and the National Australia Bank (A$500 million), which on-lent the proceeds to companies implementing strong gender equality policies such as promoting women in executive positions. The World Bank and IFC have issued several gender bonds. The Sustainable Stock Exchange Initiative has issued guidelines on how stock exchanges can promote gender finance, for example through improved disclosure and metrics for listed companies. Gender equality bonds are also being issued as “social bonds”.

[10] Social or Environmental Impact Bonds (S/EIBs) are another type of blended finance. These bonds, more appropriately and increasingly called “pay for success financing”, lay out the intended impact from the start. Investors invest because they support the goal and believe the impact can be achieved. They are repaid to the extent the impact is met. The entity that repays the investor is often a government that benefits from the achieved impact, e.g., through financial savings or meeting environmental regulatory requirements.

[11] International financial institutions like the International Finance Corporation (IFC), Asian Development Bank, KfW in Germany, Overseas Private Investment Corporation (OPIC) in the U.S., and the Netherland’s FMO (Development Finance Company) are the largest investors in blended finance transactions in emerging markets.

[12] Toronto Centre, Climate Change, TC Note (July 2017), https://www.torontocentre.org/index.php?option=com_content&view=article&id=74:climate-change&catid=14&Itemid=101#:~:text=Climate%20Change&text=Toronto%20Centre%20provides%20high%20quality,advance%20financial%20stability%20and%20inclusion., provides an extensive discussion of the TCFD.

[13] United National Environment Programme, Sustainable Insurance: The Emerging Agenda for Supervisors and Regulators, August 2017, p. 7, https://www.unepfi.org/psi/wp-content/uploads/2017/08/Sustainable_Insurance_The_Emerging_Agenda.pdf. The UN also reports that only 20% of global premium volume is covered by companies that have signed the Principles for Sustainable Insurance (PSI).

[14] See Toronto Centre, Climate Change, TC Note (July 2017), https://www.torontocentre.org/index.php?option=com_content&view=article&id=74:climate-change&catid=14&Itemid=101#:~:text=Climate%20Change&text=Toronto%20Centre%20provides%20high%20quality,advance%20financial%20stability%20and%20inclusion., for a more extensive discussion.

[15] The Sustainable Stock Exchange Initiative convenes stock exchanges worldwide to identify how exchanges, in collaboration with investors, regulators, and companies, can strengthen ESG transparency and encourage sustainable investment. It is organized by the Unite Nations Conference on Trade and Development (UNCTAD), the United Nations Global Compact, the United Nations Environment Programme Finance Initiative (UNEP FI), and the Principles for Responsible Investment (PRI). See www.sseinitiative.org.

[16] The concern has been that incorporating ESG analyses competes with the fiduciary responsibility to optimize financial returns – that there is a tradeoff between doing good and doing well financially. Increasingly the view is that ESG factors influence an investment’s financial strength in the future if not today, that they need to be included in the investment analysis, and that not including them can be a failure of fiduciary duty. See United Nations Environment Program, Fiduciary Duty in the 21st Century (2015), https://www.unepfi.org/fileadmin/documents/fiduciary_duty_21st_century.pdf.